The Nec Standard Form of Contract and Its Application to Project Managers

In this, the second ina series of articles on the NEC standard form of contract, we again look at asituation ...

The Local Government Authority have previously estimated that Local Authorities spend around £650 million annually on insurance premiums. The exact cost of insurance could now be significantly higher. By adopting a mutual model, there is an opportunity to target annual savings of up to 20%. This could potentially save over £100 million each year – or more than £500 million over a five-year budget.

The actual savings will depend on the specifics of claims, but even a conservative estimate of a 12.5% saving on a £650 million annual bill could lead to £75 million in savings (or £375 million over five years), easing the financial burden that is part of the increased pressure on council tax and the cost to individuals of Local Government.

The Local Government Association has estimated that its members are paying the insurance industry annual premiums in the vicinity of £650m. They are also paying the number of claims within their deductible, or excess, which is likely to be of a similar magnitude.

The sector’s insurance landscape is dominated by three corporate entities, one insurer in Zurich Municipal and two Managing General Agents in Risk Management Partners (RMP) (owned by Arthur J Gallagher) and Maven (owned by AON).

There are also a number of small buying groups, such as the Insurance London Consortium (ILC), they need to capture the sector’s collective scale and buying leverage.

The primary tool that Local Authorities use to cover their insurance costs is the level of self-insured deductible they choose, which has resulted in local authorities having deductibles ranging from thousands to hundreds of thousands and even to millions of pounds. The higher their magnitude, the greater their potential to generate significant balance sheet volatility for these Local Authorities (LA’s).

The new Labour government came to power on a manifesto which included a commitment to double the size of the mutual and cooperative sector. LA’s could use a mutual to offset some of the risk and reduce the cost of their current insurance arrangements.

A mutual is owned entirely by, and run for the sole benefit of, its members (in this case, it would be the LA’s themselves) and run by a board which is drawn from the membership (again, from within the LA’s themselves).

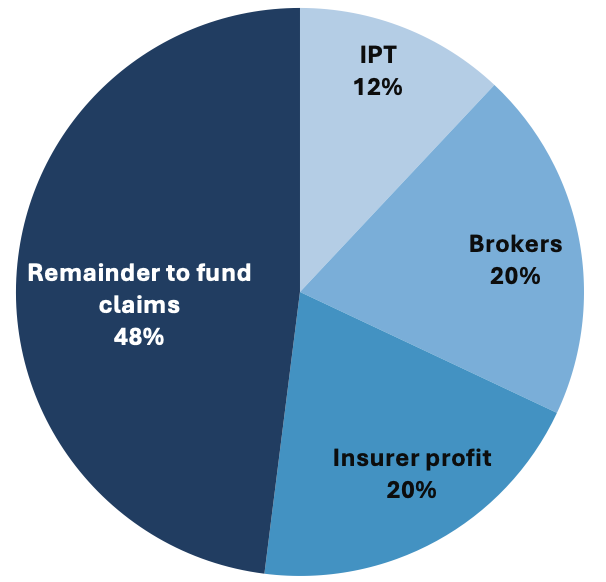

With IPT consuming 12% of insurance expenditure, if your insurance broker / MGA is earning 20% in fees, commissions and other charges, and if the insurer providing the capacity is targeting a 20% profit margin to satisfy the needs of its shareholders, then less than half of what local authorities are currently paying would actually remain available to fund the cost of claims, the majority having been siphoned off to fund causes other than the insured’s claims.

Removing these costs gives the mutual the clear potential to deliver significant savings and provide higher quality outcomes / advantages that also provide indirect savings.

Yes. Municipal Mutual Insurance (MMI) operated successfully from 1903 to 1990. Claims between 1990 and 1992 caused net assets to fall below the minimum regulatory solvency requirements, and it subsequently ceased writing or renewing business. In its latter years, MMI began writing about non-local authorities’ businesses locally, and internationally. Claims from these placements, rather than its core local authority business contributed to its demise. Zurich acquired this book of business which forms the basis for Zurich Municipal.

The main issues which brought about MMI’s demise would not affect a new mutual for LA’s:

In 2007, London Authorities Mutual (LAML) was created, operating successfully until RMP brought a legal case against one of its members, Brent, alleging that Brent’s participation in LAML was in breach of the Public Contracts Regulations 2006. Brent lost in the High Court and the Court of Appeal, but won in the Supreme Court. By then, decision had already been made to put LAML into run-off. Due to the actions of RMP, a mutual for the fire and rescue services, FRAML, followed LAML into run-off.

The Supreme Court decision removed the issue that affected LAML and FRAML, and the ability of LA’s to participate in a mutual is now permitted by the Procurement Act 2023.

Yes, from the ashes of FRAML, rose the Fire & Rescue Indemnity Company Limited (FRIC) which has been successfully trading since 2015 and currently provides cover to 14 authority members.

The recommended structure would be a Hybrid Discretionary Mutual (the same structure which is used by FRIC (and many others)). This brings with it a number of advantages, including:

Under a Discretionary Mutual, the primary layer of risk (which attracts the highest allocation of member contributions) would be retained and dealt with in the mutual, with the balance being laid off into the commercial insurance marketplaces (absent central government support for a paid for facility).

LA’s who are willing to join the conversation and put in the time, effort and data required to bring the mutual to life. Through this they would take back ownership and control of their insurance expenditure, and thereby deliver the enduring change the sector has been calling out for.

If so, please get in touch with us at enquiries@pmm.co.uk

Get in touch to learn how mutuals offer stability, predictability, and financial efficiency in risk management.

Get in touch for a Consultation

Prospect is a multi-disciplinary practice with specialist expertise in the energy and environmental sectors with particular experience in the low carbon energy sector. The firm is made up of lawyers, engineers, insurance and risk management specialists, and finance experts.

This article remains the copyright property of Prospect Law Ltd and neither the article nor any part of it may be published or copied without the prior written permission of the directors of Prospect Law.

This article is not intended to constitute legal or other professional advice and it should not be relied on in any way.

Further Reading

In this, the second ina series of articles on the NEC standard form of contract, we again look at asituation ...

In this four-part Energy Highlights series, Energy Economist Dominic Whittome analyses the pressures shaping global energy markets in 2025. This article ...

The unanimous judgement of the UK Supreme Court in Halliburton Company -v- Chubb Bermuda Insurance Ltd (2020) UKSC 48 has attracted overwhelming ...

The buzz around governance is growing louder, the spotlight is increasingly focused on the efficacy of mutuals in sustainable energy. ...

Our economist Dominic Whittome shares the latest wholesale gas and electricity prices for power markets in the Energy Market May 2023. ...

Various cost scenarios can be run, based on projected compounding rates of inflation and forward base-load electricity prices. However, here ...