Wholesale Energy Prices: April 2022

Our Energy Economist, Dominic Whittome shares his Energy Highlights Report on oil, natural gas and electricity prices at the start ...

As a follow-up to our introductory paper on Discretionary Mutuals, Our Risk Transfer and Mitigation Specialist, David Gudopp, digs a little deeper into the rationale and advantages of retaining the primary layer of risk in a Discretionary Mutuals.

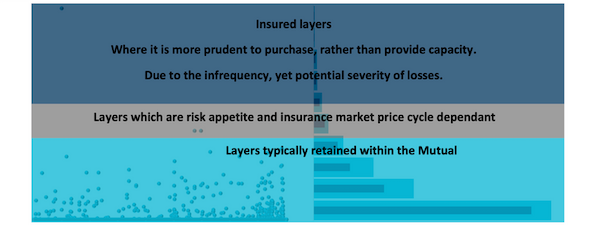

When analysing the historic claims data from potential membership groups, what we typically see is the bulk of loss cost and count [AC1] located at the base of the placement, which tapers off as you move up:

Typically, the aim of the mutual will be to retain all of the ‘expected’ losses within the mutual, whilst arranging excess layer insurance for individual losses beyond the discretionary mutuals retention.

Having determined the per claim discretionary mutuals retention, we are then able to look at the historic retained claims accumulations based upon that level of retention, adding a buffer margin, to again, ensure that the mutual retains the ‘expected’ losses, whilst arranging insurance for the ‘unexpected’ losses:

Collectively, these insurance placements combine (either on a per class with an excess drop-down or cross-class aggregate basis), to enable the mutual to accurately quantify the retained claims exposure, thereby ensuring that this remains within the risk appetite of the mutual.

Value erosion:

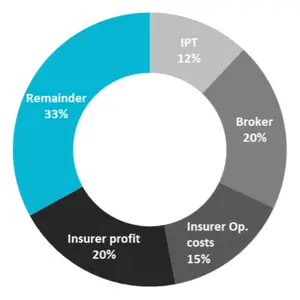

The primary risk transfer path used by the majority of businesses is to engage a corporate insurance broker to place their covers with a corporate insurer.

For illustrative purposes, if we assume:

Collectively, these consume a significant proportion of the premium, materially eroding what is left to actually pay claims.

Collectively, these consume a significant proportion of the premium, materially eroding what is left to actually pay claims.

In such circumstances, whilst the gross loss ratio (total premium paid divided by the cost of claims), may generate a perfectly acceptable loss ratio (well below 100%). When the same equation is applied to the net premiums actually received by the insurer (from which claims are funded), what initially appeared to be a profitable policy for the insurer, is in fact running below their targeted outcome, warranting corrective action.

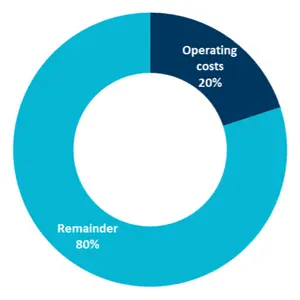

Mutual operating costs come in below the combined total of insurer operating costs and the mandatory profit margin (which is inherent

in the corporate insurer model to satisfy their shareholders)

In the above circumstances, a significantly higher proportion of the funds remain available to pay claims, evidencing how, based on the same expenditure, the result can be transformed.

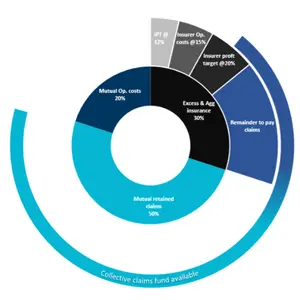

In turn, the above factors evidence the vital importance of understanding the frictional costs which are present in any placement chain, and the viability of transferring expected claims into the selected framework. The optimal outcome should become increasingly nuanced and blended.

When an illustrative allocation for the Discretionary Mutuals excess and aggregate insurance purchases is added to the equation, we can see that the proportion of member expenditure would remain

available to fund the cost of claims (both in their mutual and within the supporting insurer), collectively remains at a significantly higher proportion than that which is shown in the initial value erosion graphic.

In addition to assisting in the attainment of these frictional and structural efficiencies, a further significant advantage is derived through the following elements:

For a community-based Discretionary Mutuals, which would typically be focused on a specific industry, when looking at the sector in its entirety, it can often be observed that 80% of all claims will be generated by only 20% of the sector (Pareto’s Law).

Insurers typically sector rate, setting occupation-based rates which are set at a level which aims to achieve the targeted level of profitability to satisfy their shareholders. Whilst an upwards pricing adjustment is made for those with a poor loss experience, typically there remains a significant amount of cross-subsidisation, with the well-managed, well-performing participants, subsidising the performance of the less well-managed, less well-performing participants.

Typically, the participants within the mutual sector are far more adept at separating the ‘good’ operators from the ‘poor’ operators. Identifying what the differences are between these two groups and setting the entry parameters for the mutual in a manner which only permits entry to the 80%. The 20% of poor performers should be precluded until such time as they are willing to adopt the risk management standards and generate the outcomes of the 80%.

This aspect on its own has the potential to positively transform results by minimising the exposure to claims of the few, whilst impacting the cost of cover for the many.

The board of the mutual typically adopts a pricing strategy which ensures that each member is rated as accurately as possible on the risk they bring to the mutual. Whilst there will be short-term fluctuations, in the long term the aim should be to ensure that there is no cross-subsidisation between members.

With a similar risk and loss profile, a larger account will typically secure lower rates from the insurance marketplace than smaller accounts are able to achieve.

Instead of the members going into the insurance marketplace one by one, the mutual is able to harness their collective group buying leverage.

Retaining a higher level of risk collectively in their mutual, than would be prudent for any of them to retain individually.

Taking the remainder of the risk into the insurance marketplace, as a single collective placement, the attraction of the combined premium pool and higher attachment points collectively, targeting the delivery of a sustainable outcome which is superior to that which would be available to them on an individual basis.

a) between the member and their mutual

The members of the mutual have a direct vested interest in the outcome. They collectively own the mutual and they collectively control it; the result (good or bad) flows to them.

The higher the level of claims the mutual experiences, the more it will need to collect from its membership. Conversely, the lower the level of claims, the less the mutual need to collect from them. This inherent self-serving interest focuses the attention of the members and the membership on the identification and application of best practices of risk management and risk mitigation.

Members will be fully aware that on retained claims, they are spending their own money. This creates an inherently positive feedback loop, proactively supporting risk management and risk mitigation (and risk selection).

Contrast this against insurance, when the value of insurance can be measured by the level of claims able to be recovered from it, creating a negative feedback loop.

This all underpins the old underwriting mantra of: “If you want to reduce the cost of cover, what are you doing to increase the quality of the risk?”

b) between the mutual and its insurer

With the membership of the mutual motivated to adopt a more proactive stance towards risk selection, management and mitigation, underpinned through the retention of ‘expected’ claims within the Discretionary Mutuals, this creates an alignment of interests between the mutual and its supporting insurer. This relationship is similar in nature to that which exists between an insurer and its supporting reinsurers – both have a vested interest in the delivery of a sustainable outcome.

If it doesn’t work for the insurer, then it doesn’t work for the mutual. If it doesn’t work for the mutual, it doesn’t work for the mutual’s membership. The interests of all parties are closely aligned for mutual benefit.

As our Risk Mitigation and Transfer Specialist in our Insurance, Mutuals and Risk Management division, David will bring over 20 years of experience to the table. David’s focus is on providing clients with an independent assessment of their risk transfer arrangements and driving targeted outcomes.

Prospect is a multi-disciplinary practice with specialist expertise in the energy and environmental sectors with particular experience in the low carbon energy sector. The firm is made up of lawyers, engineers, insurance and risk management specialists, and finance experts.

This article remains the copyright property of Prospect Law Ltd and neither the article nor any part of it may be published or copied without the prior written permission of the directors of Prospect Law.

This article is not intended to constitute legal or other professional advice and it should not be relied on in any way.

Further Reading

Our Energy Economist, Dominic Whittome shares his Energy Highlights Report on oil, natural gas and electricity prices at the start ...

On 5th May 2020, the Second Senate of the BvfG returned its verdict and granted the constitutional complaints of the claimants ...

In recent years some activists have honed their tactics with a view to causing as much disruption as possible to ...

In this article, Dominic Whittome covers recent changes to wholesale energy prices. Crude Oil Oil prices rose another 22% over the ...

A modern workplace stands out for protecting its employees using respectful policies and processes which reflect the organisation's position on ...

From 1st April 2025, cruise ships docking in Rotterdam will be able to draw their energy directly from the quay, thanks ...