German Court's May 5th Judgment: Boon or Bust for Eurosceptics?

On 5th May 2020, the Second Senate of the BvfG returned its verdict and granted the constitutional complaints of the claimants ...

Last Wednesday, David Gudopp had the opportunity to present at the WFAA (Waste Facilities and Asset Association) event, where he discussed a critical issue affecting many industries, particularly waste management: the inefficiencies baked into traditional insurance models and how to entities can cut corporate insurance costs.

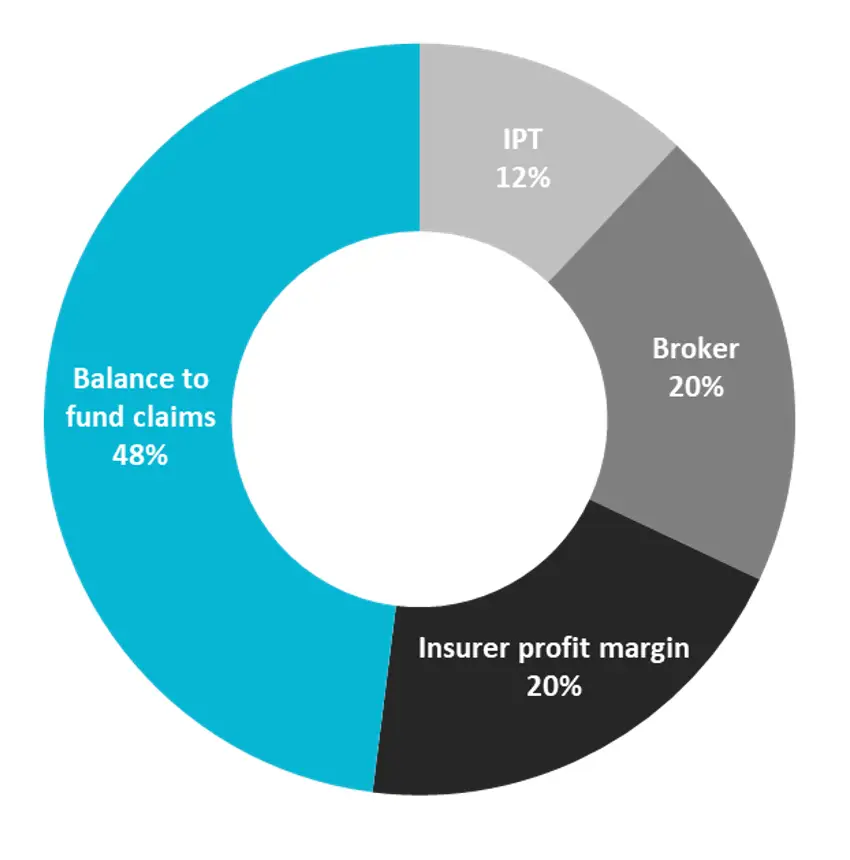

In this article, David examines how traditional insurance premium structures – loaded with taxes, broker fees, and insurer profit margins – can result in less than half of the cost being available to pay claims.

When analysing the breakdown of insurance premium expenditure, several concerning elements emerge.

With Insurance Premium Tax (IPT) currently adding 12% to the cost of cover, broker fees and commissions often accounting for another 20%, and insurers targeting a 20% profit margin to satisfy third-party shareholders, we find that less than half of the premium paid is available to cover potential claims.

For industries that regularly interact with insurers due to higher claims activity, this makes for a very inefficient structure when the cost of cover is constructed.

As the illustrative ratios show, for every £1 received in claims, businesses are required to pay £2 in premiums.

The full value of every £1 being paid into and retained by the mutual is therefore fully available to pay claims (with operating costs being a constant in both environments).

Unlike traditional insurance models, where premiums are subject to multiple layers of fees and taxes, a Discretionary Mutual offers a more streamlined and member-focused alternative:

Discretionary Mutuals have been a feature of the UK risk transfer marketplace since the 1800’s, their position being well understood and defined.

Over the past decade, new mutuals have been launched in diverse sectors, from the emergency services (FRIC) to the cryptocurrency industry (Nexus Mutual), proving that they remain versatile and effective solutions.

For sectors like waste management, where claims frequency and costs can quickly add up, the efficiencies and advantages of Discretionary Mutuals offer a compelling alternative to traditional insurance models. By eliminating unnecessary costs and providing a structure that is owned by and exists for the benefit of its members, Discretionary Mutuals are a solution well worth considering.

Get in touch to learn how mutuals offer stability, predictability, and financial efficiency in risk management.

Schedule a Consultation

Prospect is a multi-disciplinary practice with specialist expertise in the energy and environmental sectors with particular experience in the low carbon energy sector. The firm is made up of lawyers, engineers, insurance and risk management specialists, and finance experts.

This article remains the copyright property of Prospect Law Ltd and neither the article nor any part of it may be published or copied without the prior written permission of the directors of Prospect Law.

This article is not intended to constitute legal or other professional advice and it should not be relied on in any way.

Further Reading

On 5th May 2020, the Second Senate of the BvfG returned its verdict and granted the constitutional complaints of the claimants ...

The Financial Reporting Council (FRC) has released a report showing that that public companies and their investors have different views ...

Prospect Law provides a series of guidance courses covering key aspects and implications of Environmental Law. Andrew Waite, Prospect Law’...

We take a look at recent headlines in the renewable energy sector in the domestic and international markets. /*! elementor - ...

This morning we hosted a webinar that considered the rapidly emerging political consensus – amongst international bodies, national and sub-national governments, ...

Dealing with COVID, as a business, is a bit like being in economy class during a storm. We can’t ...