Mutual Insurance Case Studies: Enhancing Business Stability

Download Now For Free Discover the Benefits of Discretionary Mutuals for Your Business Are you looking to achieve operational efficiency, ...

Discover the pros and cons of a Group Company Discretionary Mutual versus a Captive Insurance Company in our latest blog. Explore key considerations for risk management and insurance strategies.

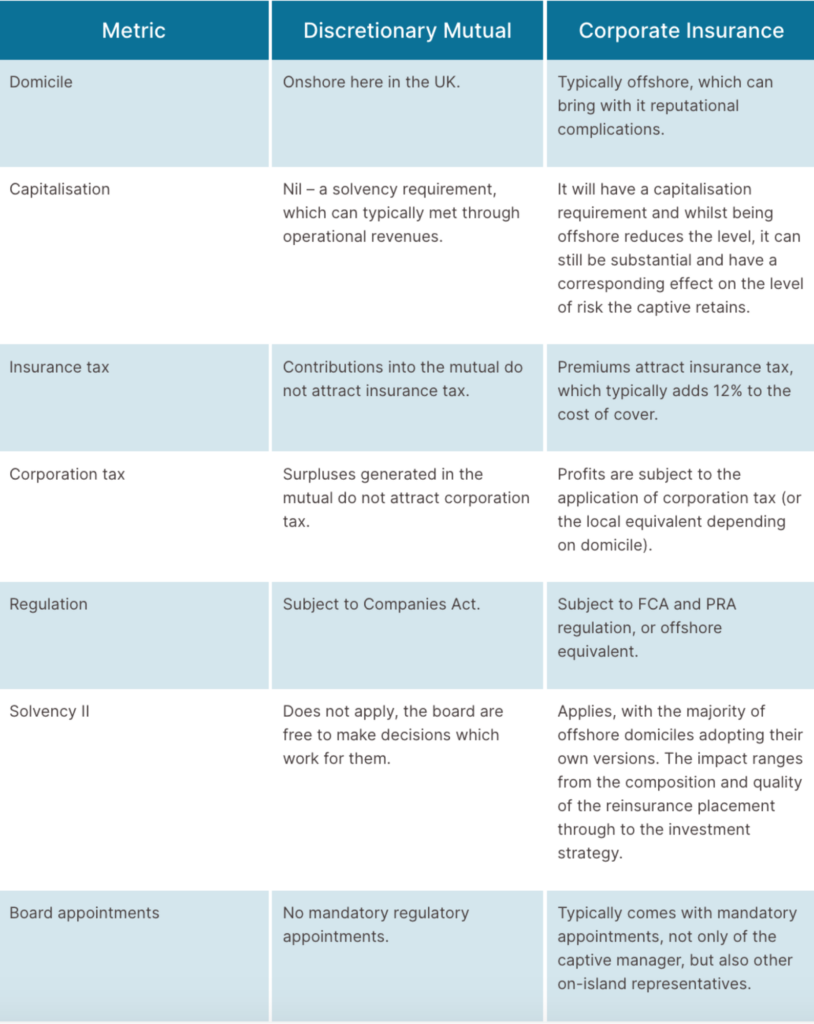

The table below aims to highlight the key differences between the operation of a Group Company Discretionary Mutual from that of a Captive Insurance company, seen from the viewpoint of the group company.

Domicile

Onshore here in the UK.

Typically offshore, which can bring with it reputational complications.

Capitalisation

Nil – a solvency requirement, which can typically met through operational revenues.

It will have a capitalisation requirement and whilst being offshore reduces the level, it can still be substantial and have a corresponding effect on the level of risk the captive retains.

Insurance tax

Contributions into the mutual do not attract insurance tax.

Premiums attract insurance tax, which typically adds 12% to the cost of cover.

Corporation tax

Surpluses generated in the mutual do not attract corporation tax.

Profits are subject to the application of corporation tax (or the local equivalent depending on domicile).

Regulation

Subject to Companies Act.

Subject to FCA and PRA regulation, or offshore equivalent.

Solvency II

Does not apply, the board are free to make decisions which work for them.

Applies, with the majority of offshore domiciles adopting their own versions. The impact ranges from the composition and quality of the reinsurance placement through to the investment strategy.

Board appointments

No mandatory regulatory appointments.

Typically comes with mandatory appointments, not only of the captive manager, but also other on-island representatives.

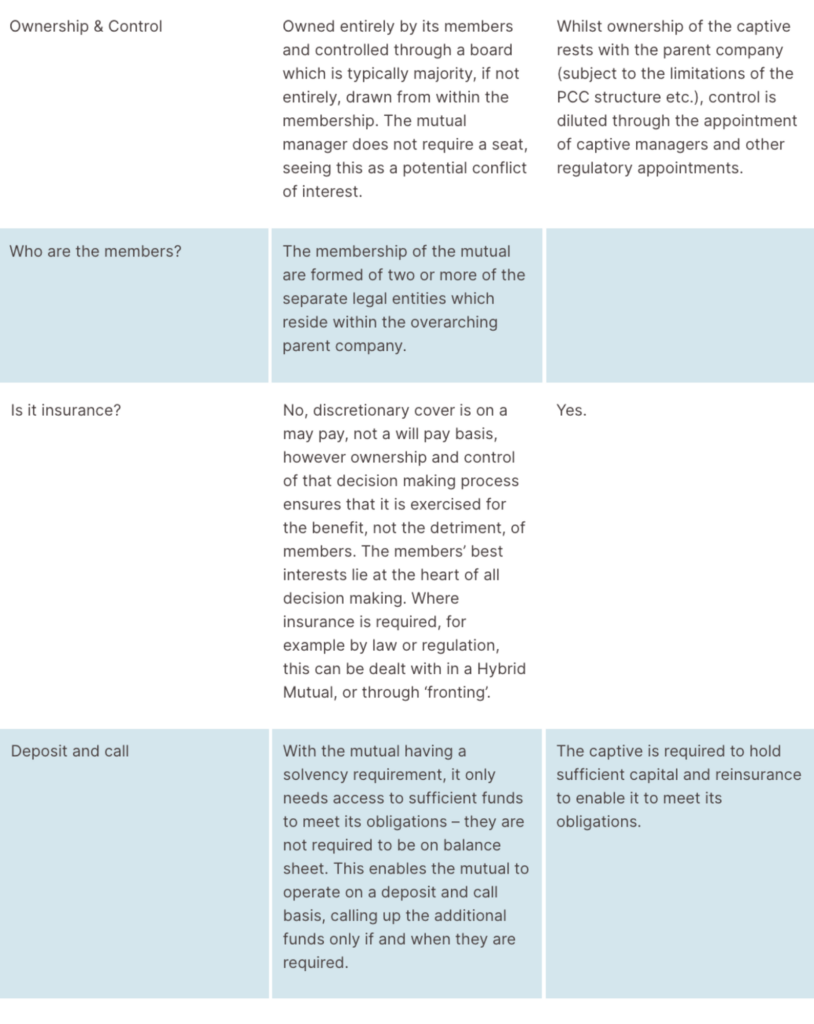

Ownership & Control

Owned entirely by its members and controlled through a board which is typically majority, if not entirely, drawn from within the membership. The mutual manager does not require a seat, seeing this as a potential conflict of interest.

Whilst ownership of the captive rests with the parent company (subject to the limitations of the PCC structure etc.), control is diluted through the appointment of captive managers and other regulatory appointments.

Who are the members?

The membership of the mutual are formed of two or more of the separate legal entities which reside within the overarching parent company.

Is it insurance?

No, discretionary cover is on a may pay, not a will pay basis, however ownership and control of that decision making process ensures that it is exercised for the benefit, not the detriment, of members. The members’ best interests lie at the heart of all decision making. Where insurance is required, for example by law or regulation, this can be dealt with in a Hybrid Mutual, or through ‘fronting’.

Yes.

Deposit and call

With the mutual having a solvency requirement, it only needs access to sufficient funds to meet its obligations – they are not required to be on balance sheet. This enables the mutual to operate on a deposit and call basis, calling up the additional funds only if and when they are required.

The captive is required to hold sufficient capital and reinsurance to enable it to meet its obligations.

It is also worth noting that when constructing the mutual legal entity, the choice of being limited by guarantee or having share capital will determine whether or not it is able to be consolidated into group accounts, the decision being made by the board on the basis of which outcome is deemed most advantageous.

The capital and tax efficiency of the discretionary mutual structure, when combined with the benefits derived from ownership and the enhanced control that gives you, mean that a Group Company Discretionary Mutual can be a very powerful tool in the risk management toolbox and lead to a reduction in the cost of risk.

Prospect is a multi-disciplinary practice with specialist expertise in the energy and environmental sectors with particular experience in the low carbon energy sector. The firm is made up of lawyers, engineers, insurance and risk management specialists, and finance experts.

This article remains the copyright property of Prospect Law Ltd and neither the article nor any part of it may be published or copied without the prior written permission of the directors of Prospect Law.

This article is not intended to constitute legal or other professional advice and it should not be relied on in any way.

Further Reading

Download Now For Free Discover the Benefits of Discretionary Mutuals for Your Business Are you looking to achieve operational efficiency, ...

The Financial Reporting Council has started to provide guidance on ESG data and how it can be collected and used. ...

Tokyo Electric Power Company Holdings (TEPCO) has begun the controversial discharge into the sea of radioactively tritiated water arising from ...

A position paper on the latest UK energy package, written by our energy economist Dominic Whittome and energy market advisor ...

Our monthly overview of our work activity, recent instructions and firm news. /*! elementor - v3.16.0 - 14-09-2023 */.elementor-heading-title{padding:0;...

‘The insurer utterly abandoned us and sought to mitigate their losses to zero’. These words, spoken by Mr Murray Pulman [1] ...