Court Convicts Directors in Brent Highway Obstruction Case

Brent Council successfully prosecuted the directors of Mizen Design Build Ltd for the wilful obstruction of the public highway under ...

In the complex landscape of risk management, businesses often find themselves at a crossroads when considering insurance options. Two prominent choices emerge: discretionary mutuals and corporate insurance. Each avenue presents distinct advantages and disadvantages, necessitating a thorough understanding to make informed decisions tailored to organizational needs. Corporate Insurance.

The table below aims to highlight the key differences between the operation of a Discretionary Mutual from that of a corporate insurance company from the perspective of the person or company buying risk cover.

![]()

Placement chain

Members typically deal directly with their mutual.

Policyholders are typically placed via brokers and MGA’s who typically earn commissions of 20-30%.

Capitalisation

Nil – a solvency requirement, which can typically met through operational revenues.

An onerous capitalisation requirement, typically in the tens of millions, attracting return on investment requirements.

Insurance tax

Contributions into the mutual do not attract insurance tax.

Premiums attract insurance tax, which typically adds 12% to the cost of cover.

Corporation tax

Surpluses generated in the mutual do not attract corporation tax.

Profits are subject to the application of corporation tax.

Regulation

Subject to companies act.

Subject to FCA and PRA regulation.

Ownership & Control

Owned entirely by its members and controlled through a board which is typically majority drawn from within the membership.

Owned by its shareholders and controlled through a board primarily comprised of representatives of those shareholders.

Alignment of interests

By the members, for the members. An entirely symbiotic relationship.

The Interests of shareholders and the interests of policy holders are frequently diametrically opposed.

Customer satisfaction

Satisfaction as measured by retention in a mutual environment is typically in the mid to high 90’s, some even attaining 100% retention rates year after year.

Lapse rates vary by class of cover and insurer, but are typically in the 80’s. Having to write that level of new business to attain revenue standstill generates significant cost.

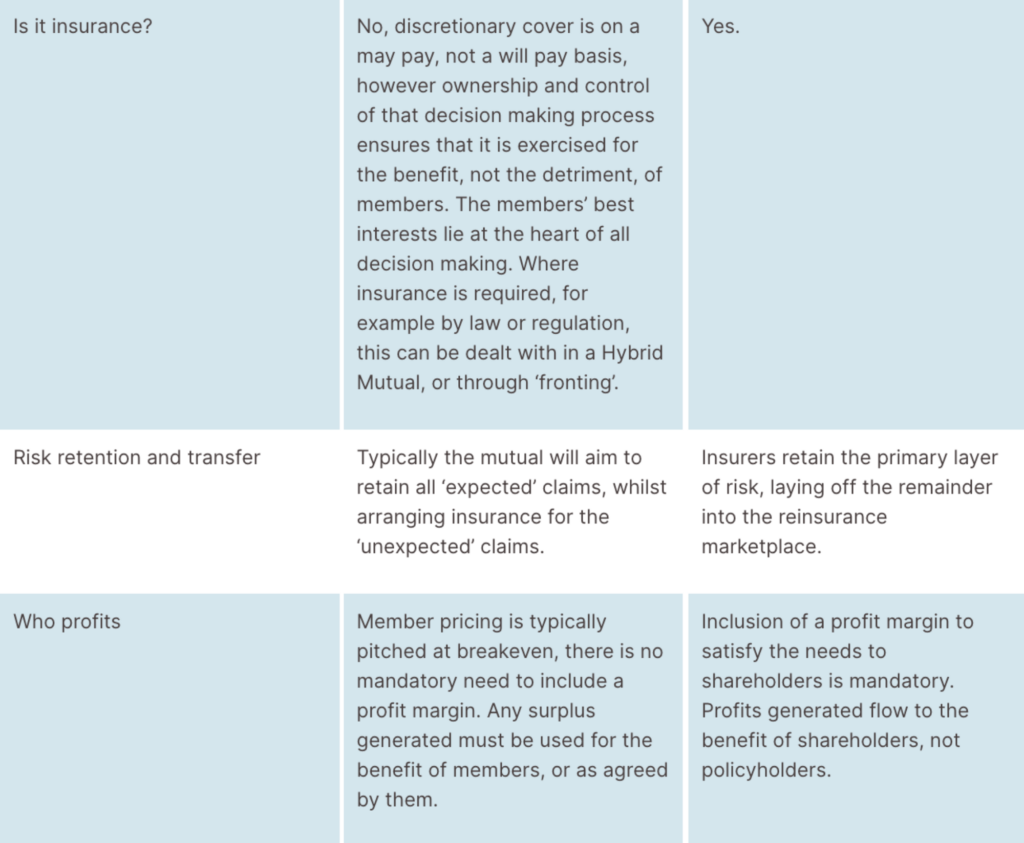

Is it insurance?

No, discretionary cover is on a may pay, not a will pay basis, however ownership and control of that decision making process ensures that it is exercised for the benefit, not the detriment, of members. The members’ best interests lie at the heart of all decision making. Where insurance is required, for example by law or regulation, this can be dealt with in a Hybrid Mutual, or through ‘fronting’.

Yes.

Risk retention and transfer

Typically the mutual will aim to retain all ‘expected’ claims, whilst arranging insurance for the ‘unexpected’ claims.

Insurers retain the primary layer of risk, laying off the remainder into the reinsurance marketplace.

Who profits

Member pricing is typically pitched at breakeven, there is no mandatory need to include a profit margin. Any surplus generated must be used for the benefit of members, or as agreed by them.

Inclusion of a profit margin to satisfy the needs to shareholders is mandatory. Profits generated flow to the benefit of shareholders, not policyholders.

The capital and tax efficiency of the discretionary mutual structure, the reduced frictional costs in the placement chain, when combined with the benefits derived from ownership and control, mean that a mutual remains a compelling and powerful proposition over Corporate Insurance.

Prospect is a multi-disciplinary practice with specialist expertise in the energy and environmental sectors with particular experience in the low carbon energy sector. The firm is made up of lawyers, engineers, insurance and risk management specialists, and finance experts.

This article remains the copyright property of Prospect Law Ltd and neither the article nor any part of it may be published or copied without the prior written permission of the directors of Prospect Law.

This article is not intended to constitute legal or other professional advice and it should not be relied on in any way.

Further Reading

Brent Council successfully prosecuted the directors of Mizen Design Build Ltd for the wilful obstruction of the public highway under ...

Australia’s stance on civil domestic nuclear power has taken asurprising turn in recent days, with the announcement by the ...

On 11th April 2022, the new Global Business Mobility visa was introduced. This visa route provides five different ways for overseas ...

/*! elementor - v3.16.0 - 14-09-2023 */.elementor-heading-title{padding:0;margin:0;line-height:1}.elementor-widget-heading .elementor-heading-title[class*=elementor-size-]>a{color:inherit;font-size:inherit;line-height:...

What, you may ask, is the relationship between crocodiles, cattle and nuclear energy?The answer lies in people - and ...

The ESG landscape has become increasingly vast and complex. There are now a great number of ESG initiatives and reporting ...