Wholesale Energy Prices: Oil, Natural Gas and Electricity as at January 2021

In this article, Dominic Whittome covers recent changes to wholesale energy prices. Oil Energy prices continued to climb across the ...

In the spring of 2011, I came to the UK to assist a Chinese client in negotiating and completing the acquisition of a European group of companies which was headquartered in the UK. At that time, the Chinese “Belt and Road” Initiative had not been initiated, and the momentum for Chinese companies to invest in the UK and other countries was just starting to really build up.

I came to the UK once again in the summer of 2011 to discuss an antidumping case with UK representatives at the EC anti-dumping committee. At that time, trade volumes between the EU (including the UK) and China were rapidly growing. By the summer of 2015, the then Prime Minister David Cameron was heralding a “Golden Era” for the developing trade and investment relationship between the UK and China.

How dramatically things have changed in just a decade: the UK has left the EU, is struggling to deal with the COVID-19 pandemic (together with the rest of the world), and appears to be on the verge of a virtual “cold war” with China, with trade and investment volumes between the two countries becoming a cause of real political and media concern.

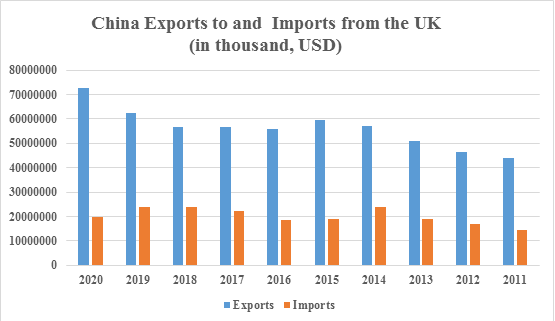

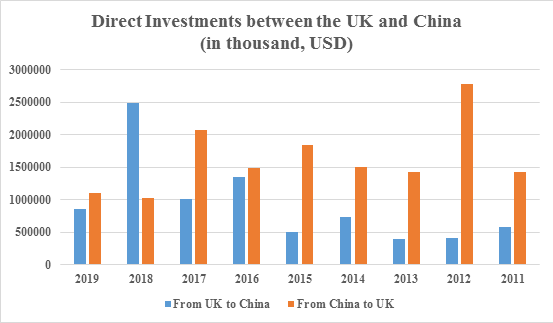

Surge of Trade and Investment Activities between the UK and China

Let’s check some statistics:

Source: National Bureau of Statistics of China, and General Administration of Customs (Data for 2020), China

Source: National Bureau of Statistics of China. Data for 2020 is not available yet.

The figures clearly demonstrate that the total value of trade between the UK and China reached USD 92,368,670,000 in 2020, with plenty of room for the UK to increase its exports to China; and the total investment value between the UK and China peaked at USD 3,508,280,000 in 2018, despite a drastic drop in 2019.

Need for a UK-China Free Trade Agreement

A free trade agreement (“FTA”) between the UK and China has been proposed in the course of the UK’s long negotiations to sort out its departure from the EU. A UK – China FTA could deal with market access, tariff concessions, trade in goods, trade in services, subsidies, investments, intellectual property protection and all other trade and investment related topics, and it would potentially serve of course to greatly increase trade and investment flows between the contracting parties.

To this point, there has been only a bilateral investment treaty (“BIT”) which was signed between the UK and China back in 1986, and which is now clearly insufficient for the substantially increased level of trade and investment activities which has grown up between the UK and China.

In contrast, the EU and China was able to reach in principle at least a Comprehensive Agreement on Investment (“CAI”) towards the end of 2020. The CAI lives up to its name – it is indeed “comprehensive” in that it contains not only investment protection provisions that are typically included in today’s BITs, but also market access, sustainable development and other provisions which are normally seen in FTAs.

The CAI, if finalized and approved by both the EU and China, would therefore provide a solid legal basis for the future material increase of trade and investment flows between the EU and China.

A UK-China CAI?

As discussed above, the protection and encouragement of trade and investment activities between the UK and China is governed at present only by the existing 1986 UK-China BIT.

The 1986 UK-China BIT is outdated and unsuitable in a number of ways, and is in urgent need of updating. A modernized BIT such as the EU-China CAI would contain detailed provisions on national treatment (NT), most-favored nation treatment (“MFN”), fair and equitable treatment, full protection and security, freedom of transfer of funds, prohibition against unreasonable, arbitrary or discriminatory measures, prohibition of performance requirements, reasonable compensation for expropriation, facilitation of personnel entry and sojourn, transparency of laws and regulations, investor-state dispute settlement (ISDS), and other progressive provisions.

Although it does contain some provisions dealing with these issues, the 1986 UK-China BIT fails to set them out in a suitably modern and comprehensive manner. For example:

It is assumed that increased trade and investment activities necessitate increased treaty protection and facilitation. FTAs and BITs are usually the appropriate mechanisms by which such treaties can most appropriate be negotiated and concluded.

However, an FTA, such as the RCEP, CPTPP and EU-Canada CETA, could take a number of years to negotiate and approve. A BIT, on the other hand, could be negotiated and approved far more quickly. With the 1986 UK-China BIT in force, and the EU-China CAI as a model, the UK and China could negotiate and approve a UK-China CAI relatively efficiently. Given the rather difficult and time consuming approval procedures at the EU, it is clearly not impossible for such a UK-China CAI to be concluded and approved before the EU-China CAI. The only prerequisite is, of course, the political will and determination to make things happen on both sides.

About the Author

Eric Jiang advises and assists clients in matters relating to customs and international trade, international investments and transactions, and international arbitration. He is licensed to practice law in New York/USA, in Ontario/Canada and in all the Provinces in mainland China. Eric studied and researched law for fourteen years in three well regarded law schools, achieving an LL.B. and M.Jur. at Peking University, an LL.M. at Queen’s University, and a J.D. at York University. He was a full-time faculty member of the School of Law at Peking University, but has since been practicing law within and outside China. Over the years, in addition to other international work, Eric has represented many companies in antidumping, countervailing and other trade remedy cases and has developed solid expertise in customs and trade laws, FTA and WTO laws.

Prospect Law is a multi-disciplinary practice with specialist expertise in the energy, infrastructure and natural resources sectors with particular experience in the low carbon energy sector. The firm is made up of lawyers, engineers, surveyors and other technical experts.

This article remains the copyright property of Prospect Law Ltd and Prospect Advisory Ltd and neither the article nor any part of it may be published or copied without the prior written permission of the directors of Prospect Law and Prospect Advisory.

This article is not intended to constitute legal or other professional advice and it should not be relied on in any way.

For more information or assistance with a particular query, please in the first instance contact Eric Jiang on +44 (0)20 7947 5354 or by email on ejj@prospectlaw.co.uk.

Prospect is a multi-disciplinary practice with specialist expertise in the energy and environmental sectors with particular experience in the low carbon energy sector. The firm is made up of lawyers, engineers, insurance and risk management specialists, and finance experts.

This article remains the copyright property of Prospect Law Ltd and neither the article nor any part of it may be published or copied without the prior written permission of the directors of Prospect Law.

This article is not intended to constitute legal or other professional advice and it should not be relied on in any way.

Further Reading

In this article, Dominic Whittome covers recent changes to wholesale energy prices. Oil Energy prices continued to climb across the ...

COP 26 is the 26th Conference of the Parties to the United Nations Framework Convention on Climate Change ‘UNFCCC’. It is ...

HinkleyPoint C (HPC) is a nuclear power station based on the French EuropeanPressurised Reactor design, code-named the EPR1. The project ...

Following the successful Free Trade Agreement with Japan the UK Government’s Department for International Trade is undertaking a series ...

Each day bringsfurther grim news of the spread of coronavirus in China and elsewhere; todaymentions of the virus have moved ...

Decommissioning the UK’s nuclear assets has long been a contentious issue, and the debate rages on. The costs keep ...